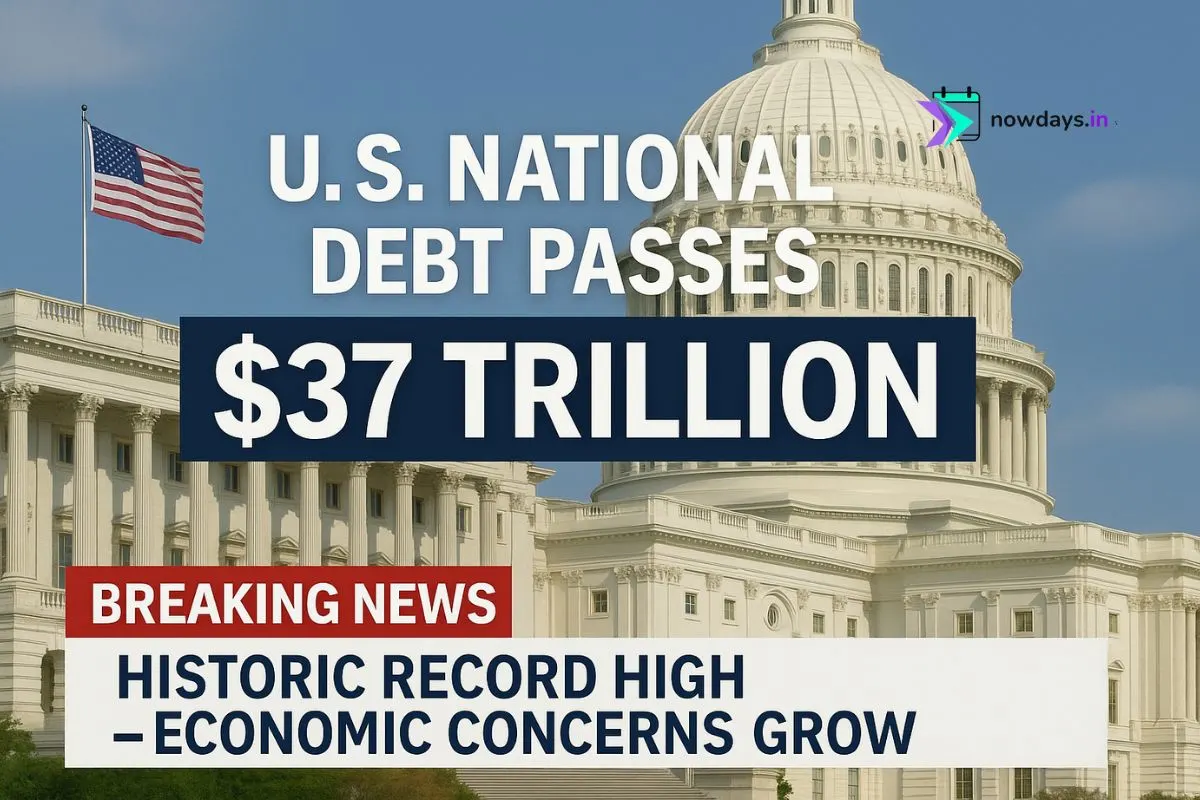

The United States’ gross national debt has effectively crossed the $37 trillion threshold, a milestone that was widely anticipated by official trackers and budget analysts through early August 2025 as borrowing needs remained elevated and interest costs surged. Treasury and congressional dashboards showed total gross debt near $36.93 trillion as of August 5, with trend-based projections indicating the $37 trillion mark would be breached around mid‑August 2025, underscoring the fastest peacetime debt buildup in modern U.S. history.

Where the Debt Stands Now

- As of August 5, 2025, total gross national debt stood at $36.93 trillion, according to the U.S. Congress Joint Economic Committee’s debt dashboard.

- Based on the 12‑month pace, the same JEC analysis projected the debt would reach $37 trillion by roughly August 17, 2025, marking an increase of about $1.87 trillion year over year.

- Treasury’s official fiscal data guide confirms debt service has ballooned: maintaining the debt cost $921 billion as of June 2025, representing 17% of total federal outlays in FY2025, a reflection of higher interest rates and a larger debt stock.

Why Debt Is Rising So Fast

- Persistent primary deficits: The Bipartisan Policy Center’s deficit tracker shows a larger FY2025 deficit trajectory than last year, leaving the Treasury to borrow heavily to finance the gap.

- Structural drivers: The Congressional Budget Office (CBO) projects that spending on Social Security, Medicare, and rising interest costs will continue to outpace revenues under current law, pushing debt held by the public from about 100% of GDP in FY2025 toward 107% by 2029 and 156% by 2055.

- Higher interest rates: With policy rates elevated, interest payments have become one of the fastest‑growing federal expenses, crowding out other priorities and amplifying the compounding effect of new borrowing on total debt service.

How Fast Is It Growing?

- Over the past year, gross debt grew by $1.87 trillion, averaging an increase of roughly $5.13 billion per day, $213.6 million per hour, and nearly $59,335 per second, per JEC’s July update.

- On a per‑household basis, the increase over the year amounts to about $14,153, taking total gross debt owed to an estimated $279,319 per household as of early August, highlighting the scale of obligations in relatable terms.

Debt-to-GDP: The Bigger Picture

- Debt held by the public—what economists focus on for sustainability—remains on an upward path and is projected by CBO to set new records relative to GDP later this decade, even before aging‑related spending pressures fully intensify.

- Longer term, CBO’s 30‑year outlook shows debt held by the public climbing to 156% of GDP by 2055 absent significant policy changes, raising the risks of slower growth and reduced fiscal space during shocks.

The Cost of Carry: Why Interest Now Matters More

- With interest costs nearing $1 trillion annually, the U.S. is spending more on servicing existing debt than many major program areas—making the fiscal arithmetic progressively harder as each new dollar of borrowing adds to future interest outlays.

- Treasury’s fiscal guide attributes 17% of FY2025 total spending to interest as of June 2025, a stark jump from the low‑rate era and a key reason analysts warn of mounting crowd‑out risks.

What Experts Are Watching

- Path of rates and growth: If nominal growth stays above effective interest rates, debt dynamics can stabilize—but CBO expects real growth to slow over the next 30 years even as interest costs remain structurally higher than in the 2010s.

- Primary balance: Stabilizing the debt ratio would require closing the primary deficit through some combination of revenue increases and expenditure restraint, an adjustment both CBO and independent fiscal groups have emphasized repeatedly.

- Timing of reforms: Analysts note that delayed action generally requires more abrupt and painful adjustments later, because compounding debt and interest reduce room to maneuver during downturns.

Investor and Market Implications

- Treasuries remain the world’s benchmark safe asset, but heavier issuance and higher rates can steepen the yield curve and tighten financial conditions, with knock‑on effects for mortgages, corporate credit, and valuations.

- Investor guidance from market strategists stresses long‑term discipline: while the debt overhang is important for policy and growth, diversified portfolios have historically navigated changing fiscal backdrops without wholesale reallocation based on headlines alone.

- Credit and ratings: Elevated debt and interest burdens have already contributed to rating concerns in recent years; sustained deterioration increases the risk of further scrutiny and higher risk premia over time.

What Could Bend the Curve

- Policy levers: Changes to benefit formulas, eligibility ages, and healthcare cost growth; broadening the tax base; and reforms that raise productivity and labor force participation can improve the long‑run debt trajectory if enacted credibly and early.

- Pro‑growth agenda: Policies that lift potential growth—targeted immigration, innovation incentives, and infrastructure productivity—can improve the denominator in debt‑to‑GDP dynamics, though they rarely substitute for budget action on their own.

- Fiscal rules: Some economists favor enforceable guardrails (e.g., spending caps paired with revenue triggers) that phase in gradually to reduce procyclicality and enhance credibility without derailing the cycle.

Bottom Line

Crossing the $37 trillion mark is a symbolic but telling waypoint: interest costs are surging, structural deficits remain persistent, and the burden is set to rise absent policy changes that align revenues and outlays over time. While markets can absorb large Treasury issuance when growth and inflation expectations are stable, the arithmetic laid out by CBO and congressional trackers makes clear that delaying fiscal adjustments increases the difficulty—and cost—of stabilization later.